》View SMM Silicon Product Prices

》Subscribe to View Historical Price Trends of SMM Metal Spot Prices

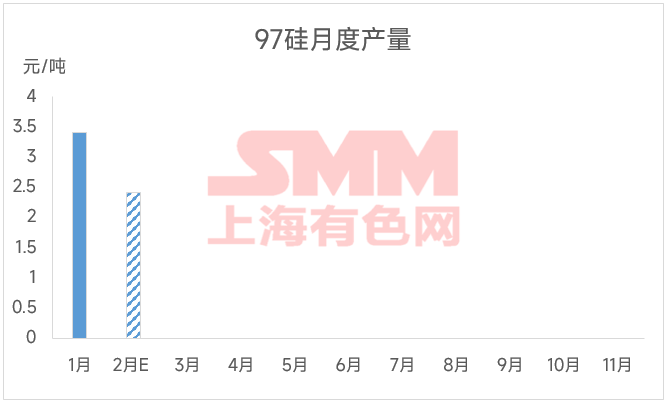

Silicon (Si≥97%) was affected by the continued weakness in the silicon metal industry, and the market performance in 2025 remained sluggish. After market prices fell below 10,000 yuan/mt, recent prices eventually stabilized around 9,500 yuan/mt. According to feedback from market enterprises, this price is near the cost line for top-tier enterprises in low electricity price regions producing silicon (Si≥97%). Most silicon (Si≥97%) enterprises have production costs above this price level. In contrast, in high electricity price regions such as Ningxia and Gansu, the cost line has long been breached, and manufacturers have been operating at a loss for some time.

Currently, the market price of silicon (Si≥97%) is below the cost line for most manufacturers. To survive and reduce losses, concentrated production cuts and production shifts occurred in January 2025. Monthly production of silicon (Si≥97%) began to decline in January, and since most production cuts occurred within January, the expected production in February saw a more significant sharp reduction. The overall expected production decreased by over 9,000 mt compared to January, down more than 20% MoM. The production cuts were relatively dispersed, with silicon (Si≥97%) plants in Ningxia and Gansu regions experiencing production cuts or shifts. According to feedback from operating manufacturers in Shizuishan, Ningxia, the current market price of silicon (Si≥97%) (1503 specification) is around 9,500 yuan/mt, which is already far below local production costs, with a loss of about 600 yuan/mt per ton. Therefore, local operating manufacturers have also reported plans for appropriate production cuts after completing production this month. As a result, the production of silicon (Si≥97%) in March may still have a slight probability of further decline.

In summary, manufacturers involved in production cuts or shifts for silicon (Si≥97%) have generally indicated no intention to resume production in the short term. Coupled with a small number of operating manufacturers still holding production cut plans in March, the supply of silicon (Si≥97%) is expected to remain below 30,000 mt per month for some time.

![Before the holiday, the black chain is unlikely to see a trend-driven market [SMM Steel Industry Chain Weekly Report].](https://imgqn.smm.cn/usercenter/zUFfM20251217171748.jpg)

![[SMM Chromium Daily Review] Inquiries and Transactions Weakened, Chromium Market Showed Mediocre Performance Before the Holiday](https://imgqn.smm.cn/usercenter/ENDOs20251217171718.jpg)